Google's stock assumes they'll dominate AI forever, which is hilarious considering Google+, Glass, Stadia, or any product launch since Gmail. Investors are betting on AI dominance from the company that killed Reader and Wave.

Google Has Real Revenue, But So What

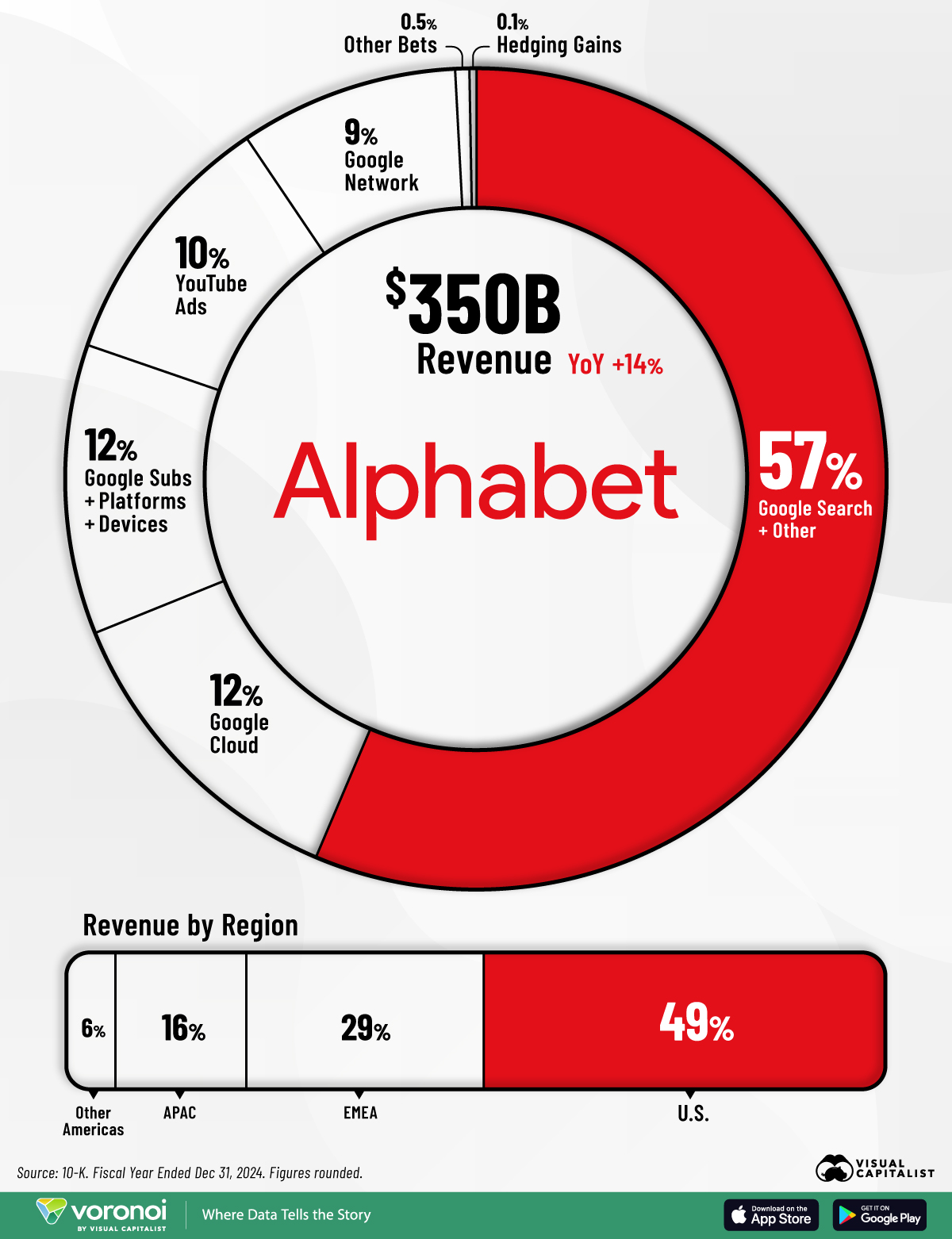

Google made $371.4 billion in 2024, mostly from search and YouTube ads. Real money, not VC promises. But they're valued like an AI startup when 80% of revenue comes from advertising when you search "pizza near me."

Gemini is decent but not revolutionary. I've used it for coding and writing - sometimes better than ChatGPT, sometimes worse. Not worth a $2.5 trillion premium.

Antitrust Relief Helped

Some regulatory pressure got lifted but that's not worth hundreds of billions in market cap. Google's search monopoly was never seriously threatened. The antitrust cases were theater about looking tough on Big Tech.

Cloud Business Still Third Place

Google Cloud is gaining on AWS and Azure but they're burning money to buy market share. Every enterprise deal probably loses money for two years. That's not sustainable growth, that's expensive customer acquisition.

Revenue Reality Check

Google makes 80% from ads. YouTube ads, search ads, display ads - all advertising. The "diverse revenue streams" bullshit falls apart when one stream dwarfs everything else.

Cloud, hardware, "Other Bets" - expensive experiments that might pay off someday. Waymo's been "almost ready" for a decade. Google hardware sells like Microsoft Zune.

This Is Bubble Territory

AI is hot so everything AI gets a premium. What happens when investors realize most AI applications are fancy chatbots that don't generate revenue? Google survives because they have search, but $3 trillion assumes AI transforms every industry simultaneously.

Sundar's "Strategic Vision"

Pichai hasn't fucked up what Larry and Sergey built, but don't confuse "not breaking Google" with visionary leadership. The big decisions - mobile, cloud, AI - were already happening when he took over.

The 15% R&D spending sounds impressive until you realize half goes to projects that die after two years. Google+? Glass? Stadia? Google's graveyard is bigger than most companies' entire catalogs.

Bottom Line

Google's a solid company with real revenue and working AI tech. But $3 trillion values them like they'll own the future of computing. That's not analysis, that's speculation.

The Real AI Problem

Google's inflated market cap is just one symptom: investors are betting trillions on AI without understanding what actually makes money.

ChatGPT writes decent emails and Gemini helps with coding. But turning that into revenue streams that justify these valuations? That's the hard part nobody wants to discuss.

Most AI applications are solutions looking for profitable problems. Google's advantage is they already have profitable problems (search, ads, cloud) and are adding AI for efficiency. That's worth something, but not an extra trillion.

Market Reality vs Hype

Wall Street analysts are pricing in AI dominance that may never materialize. Google Cloud grew 35% but still trails AWS and Microsoft Azure. The AI infrastructure costs are massive - $13.4 billion in Q3 2024 capex mostly on data centers and AI chips.

Gemini adoption is growing but monetization remains unclear. Enterprise AI services compete against OpenAI, Anthropic, and AWS Bedrock in a crowded market.

The Google Graveyard Effect

Google kills more products than I kill houseplants - Google+, Stadia, Glass, Wave. The graveyard website lists 295 discontinued products. Investors are betting this time is different because AI is the future, but Google's track record suggests they'll find a way to screw it up.